Electronic Invoicing

Why E-Invoicing?

To help improve the work process and to achieve digital transformation in the government sector, the application of the electronic invoice comes in the context of the permanent endeavors of the Zakat, Tax and Customs Authority. There are numerous benefits from using this system, such as:

- Eliminate false invoices and reduce tax evasion.

- Time and Cost Saving: With e-invoicing, we can reduce many unnecessary steps involved in the invoicing process. As a result, both the company and its customers save a lot of time by using the automated invoicing system.

- Faster settlement and less disputes: Receiving a law enforced electronic invoice (instead of a paper-based) reduces disputes regarding invoice acceptance and approval.

- Ease of saving, tracking, and mass processing of invoices: After the issuance of the invoice using the electronic invoicing system, it will be easy to track, display, and pay which helps the employee to handle / process significantly more invoices.

- High degree of control and ease of access: Because electronic invoices are saved in online platforms/databases, the user can access them from anywhere and from any device.

Aspects of Electronic Invoice

The application of electronic invoicing requires a complete review of several aspects, processes and practices in the company, including:

- An application to issue, save, and display invoices and notifications

- Network security systems, cyber security, application security, and information technology infrastructure

- The digital certificate for the invoice and for the credit and debit notes

- Tax and work procedures

- Invoice data and notifications

Application/Implementation Date:

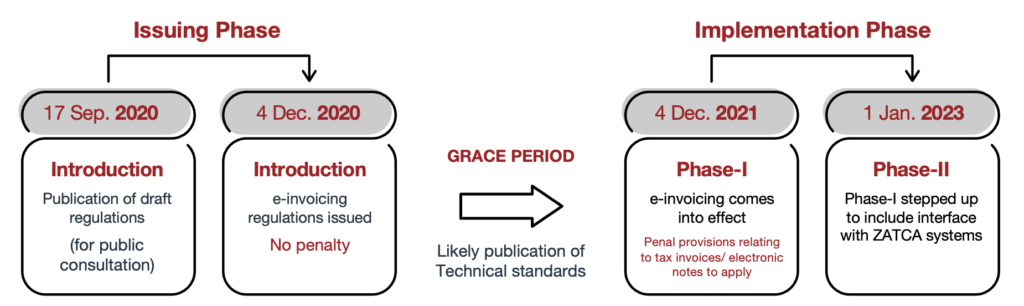

As of September 17, 2020, KSA initiated the application of electronic invoicing as a part of the issuance (phase) process. During the development and publishing of the draft regulations, the public had the opportunity to express their remarks and suggestions, and on December 4, 2020, the electronic invoicing regulations were issued. Taxpayers were given a 12-month period to prepare and implement the electronic invoice (the first implementation phase) that ends on December 4, 2021; however, the linking process with the authority’s system and some other requirements related to electronic encryption were postponed to the second phase of the implementation process, which will start on January 1, 2023. The second phase of the implementation process may begin after providing a final list and details of the segments (assignees), who are subject to implement the e-invoicing and finalize the linkage process six months before the actual application for each segment.

Our Methodology:

Andersen in Saudi Arabia’s unique approach to the implementation of electronic invoicing provides a great added value for facilities. We have a team of certified professionals with extensive experience in the field of tax advisory, and business and technology advisory – providing the adequate experience and knowledge to ensure our clients receive high-quality outputs.

Several options have been developed to choose from depending on the needs of the organizations:

Our Approach for e-invoicing: Option 1 -Assessment for the current Situation

Our Approach for e-invoicing: Option2 – Supervision

Our Approach to e-invoicing: Option3 – Supervision and implementation

Commonly Asked Questions

1. Am I subject to electronic invoicing?

All registered taxpayers (with a value-added tax file or number) are subject to the e-invoicing instructions as of December 4, 2021.

2. What are the electronic invoicing requirements?

There are several requirements to apply and fulfill the e-invoicing in the first stage (December 4, 2021), including:

i. The issued invoices must match the tax invoice and ensure its integrity in terms of values, information, and entitlement.

ii. A software that can be used for e-invoicing and notifications:

• ERP Software

• Invoicing Applications

• Point of Sale (P.O.S.)

• Handheld vending machines

iii. IT Infrastructure

iv. Network and Cyber Security

3. Is it sufficient to modify the invoice data and print the QR Code on the invoice?

In the first phase of implementation (December 4, 2021), the special requirements for the security of the database and other infrastructure must be met and the invoicing programs and their notifications must not be tampered with.

4. We have an accounting program that only one or two employees work on in the company. Is it sufficient to issue an invoice from this program?

A comprehensive assessment of the work environment and the current invoicing process must be made. It may require restructuring the tax invoice issuance process and its notifications (not only the general form of the invoice). This may require modifications to the program as well as changing the devices used (especially a printer that cannot print a QR Code). On the other hand, a contract with an IT service company for backups and system management is needed to ensure that the database is not tampered with. This may require changing the current accounting software entirely.

5. What are the requirements of the approved program for electronic invoicing?

In addition to issuing the electronic invoice, it should have the ability to store the tax invoice and its notifications electronically on a database. Also, it requires an internet connection to be able to issue files from it in the format specified by the Zakat, Tax and Customs Authority. There must be sufficient support for the program from the supplier company in case further modifications are applied during the implementation of the second stage and linking with the Authority. It is vital to ensure that there is no possibility of tampering, along with empathizing the importance of having backup copies of the data.